The most dramatic challenge to the world’s military spending equilibrium comes from the United States. US President Donald Trump has proposed boosting the defence budget to an unprecedented $1.5 trillion by 2027—a figure widely characterized as a 50%+ increase over recent plans. If enacted, this single policy would not just break America’s fiscal mould; it would threaten to shatter the fragile global plateau that has contained defence spending as a share of world GDP at around 2.5%, far below Cold War levels.

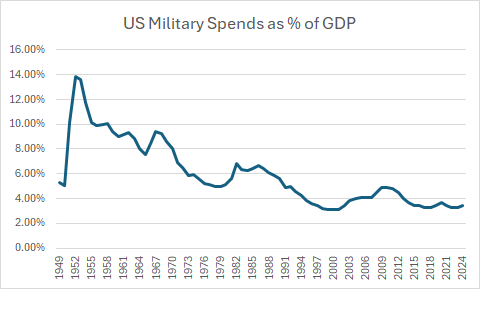

The sheer scale of the proposal is staggering. It would likely push U.S. military expenditure to between 4.8% and 5.0% of GDP, a level not seen for a decade. This would represent a seismic shift, single-handedly pulling the global average upward and applying intense pressure on allies and rivals alike to reassess their own fiscal limits. The question is no longer abstract: can political will overwhelm the economic and social constraints that have so far contained global defence spending?

The Plateau Under Pressure

As we move through early 2026, the world awaits the definitive SIPRI report on 2025’s global military expenditure (expected in April 2026). The trend, however, is already clear. Global spending is expected to have remained at or fractionally above the 2024 record level of approximately 2.5% of world GDP. This sustained elevation confirms a new, tense normal. Yet, it also underscores a powerful truth: despite record nominal spending driven by war in Europe and strategic competition in Asia, the world has not returned to the sustained Cold War benchmark of 3.5%.

| Military Spending as a % share of GDP | Change in Spending (%) | |||

| Rank | Country | 2024 | 2015 | 2023-24 |

| 1 | United States | 3.4 | 3.5 | 5.70% |

| 2 | China | 1.7 | 1.8 | 7% |

| 3 | Russia | 7.1 | 4.9 | 38% |

| 4 | Germany | 1.9 | 1.1 | 28% |

| 5 | India | 2.3 | 2.5 | 1.60% |

| 6 | United Kingdom | 2.3 | 2.0 | 2.80% |

| 7 | Saudi Arabia | 7.3 | 13.0 | 1.50% |

| 8 | Ukraine | 34.0 | 3.8 | 2.90% |

| 9 | France | 2.1 | 1.9 | 6.10% |

| 10 | Japan | 1.4 | 0.9 | 21% |

| World | 2.5 | 2.3 | 9.40% | |

| Source: SIPRI | ||||

This current plateau is significant. It represents a consolidation of the steep increases seen after Russia’s 2022 invasion of Ukraine. Major spenders have institutionalized higher budgets; Germany’s major Defence policy shift is now reflected in multi-year plans, and Eastern European nations consistently exceed NATO targets. However, the leap from today’s global 2.5% to a sustained 3.5% remains a monumental fiscal and political chasm. The spending share has hit a ceiling due to three structural constraints:

- The “Triple” Trilemma: In most developed democracies, the largest budget items—healthcare, pensions, and debt service—are politically untouchable. Concurrently, the colossal investment required for climate adaptation demands a significant share of GDP. Defence must compete in this zero-sum game.

- Fragmented Threat Perception: Today’s multipolar world creates asymmetrical priorities. While Eastern Europe’s spending soars, other regions face different pressures, preventing a synchronized global jump.

- Economic and Fiscal Realities: High post-pandemic debt burdens limit the ability to fund defence hikes through borrowing without destabilizing interest costs or forcing unacceptable trade-offs.

This is the landscape of “Peak Pressure, Not Peak Percentage.” We see record absolute spending and strained defence industries, all while the global GDP share stabilizes. Every incremental increase is fought over bitterly in domestic budgets, directly impacting investments in health, education, and climate resilience.

A Proposal to Break the Mold

The $1.5 trillion U.S. proposal is a direct assault on this trilemma. It isn’t just a large number—it’s a proposition to fundamentally reorder U.S. fiscal priorities. Funding it would require seismic shifts: catastrophic cuts to domestic programs, monumental new borrowing, or tax increases, all within a politically divided Congress. Its passage and sustainability are far from certain. But its mere proposition is a forcing mechanism, challenging the very logic of the plateau.

Simultaneously, acute regional crises are testing these limits from other directions. The India-Pakistan aerial faceoff in May 2025, set against persistent global uncertainty, has intensified domestic calls for a significant boost to India’s defence budget. Currently at 2.3% of GDP, an increase would fund accelerated modernization and indigenous production. For New Delhi, the challenge mirrors the global one: how to allocate more to security without derailing critical spending on infrastructure and social programs for a growing population.

The Battle for the Future Budget

These imminent decisions—in Washington, New Delhi, and other capitals responding to ongoing conflicts—will define the next phase. They are live experiments in whether the political will born from great-power competition and regional flashpoints can overwhelm the economic and social constraints that have contained spending shares.

In conclusion, the post-Cold War peace dividend is gone, replaced by a stubborn, high-level equilibrium. The age of austerity for other vital public goals has already begun. The defining challenge for governments in 2026 and beyond is not merely funding defence, but managing the insidious trade-offs that sustained high spending imposes on national resilience and future prosperity. The new front line is the Government finances. The battles fought there over the coming months, starting with the audacious proposal on the American table, will reveal whether the global spending plateau holds firm or finally cracks under the weight of a world that feels increasingly at war with itself.

#MilitarySpending #DefenseBudget #Geopolitics #GlobalSecurity #ForeignPolicy #DefenseIndustry #BudgetAllocation #FiscalPolicy #SIPRI #ColdWar #GDP #USPolitics #Zeitenwende #NATO #India #MakeInIndia #ClimateSecurity #DefenseNews #PolicyAnalysis