Executive Summary

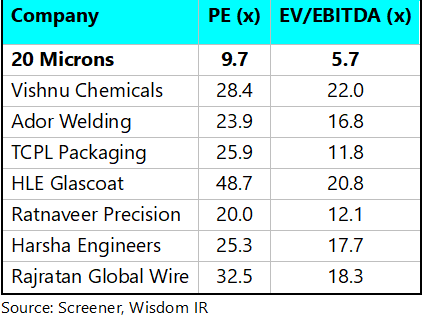

20 Microns currently trades at 9.7x PE and 5.7x EV/EBITDA on trailing basis, a substantial discount to a group of listed Indian industrial intermediate suppliers whose valuations range from 20x–49x PE and 12x–22x EV/EBITDA. Despite this discount, 20 Microns’ operating and financial performance compares favourably with most of these companies.

The market appears to view 20 Microns as a mining or commodity company. However, the company’s long-term financial record suggests that it behaves more like a specialised industrial materials company supplying critical inputs to a broad range of manufacturing industries.

The central question is simple:

Can a commodity business with no competitive advantage sustain 18% ROCE, generate over ₹330 crore of free cash flow over a decade, maintain stable profitability through cycles and simultaneously strengthen its balance sheet?

The evidence suggests the answer is no.

The Valuation Puzzle

In this note, we have taken a few industrial intermediate suppliers of diverse types. There are several other names that could be added; however, the essential insights would remain the same. 20 Microns is by far the cheapest despite comparable metrics on all fronts, as discussed in the note (an Appendix at the end has more detailed data)

The valuation discount becomes even more striking when compared against operating metrics.

20 Microns has:

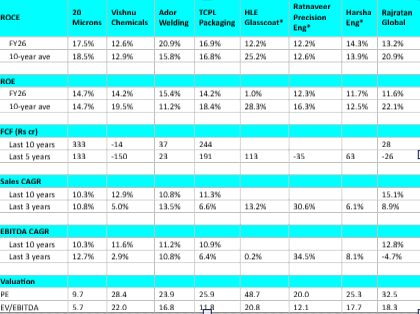

- FY26 ROCE of approximately 18%

- 10-year average ROCE of approximately 19%

- 10-year average ROE of approximately 15%

- Over ₹333 crore cumulative free cash flow generated during the past decade

- Revenue CAGR of approximately 10%

- EBITDA CAGR of approximately 10%

- Significantly improved leverage over time.

These are not the numbers of a structurally weak business.

In fact, the most striking observation from the comparison is that the gap in market valuation is considerably wider than the gap in operating fundamentals.

While 20 Microns trades at a 60-80% discount to most peers on PE and EV/EBITDA multiples, its return ratios, cash generation, balance sheet strength and growth profile are broadly comparable to many of them. The financial data suggests a modest operating gap at best, whereas the valuation gap is exceptionally large. This disconnect raises the possibility that the market is misclassifying the business rather than appropriately pricing its fundamentals

Is 20 Microns Really a Commodity Company?

This is perhaps the most important issue.

Commodity businesses typically display:

- Cyclical returns on capital

- Volatile margins

- Weak cash generation

- Periodic balance-sheet stress

- Difficulty sustaining excess returns over long periods

The reason is straightforward. If a product is truly undifferentiated, high returns attract competition and excess profits eventually disappear.

Yet 20 Microns has maintained close to 18–19% ROCE over a decade while generating meaningful free cash flow and steadily reducing financial leverage.

Such consistency usually indicates the presence of competitive advantages.

The market may be looking at the raw material and missing the value addition.

Customers do not simply buy talc, calcium carbonate or silica.

They buy:

- Particle size consistency

- Brightness and purity standards

- Functional performance

- Formulation support

- Technical service

- Reliability of supply

- Product qualification

For many end-users, changing a supplier is neither easy nor risk-free. Industrial formulations often require years of qualification and customer approval.

As a result, 20 Microns’ business economics appear much closer to those of a specialised materials supplier than a pure mining company.

Why Do Peers Command Higher Valuations?

A review of comparable companies suggests that valuation differences are driven more by market perception than by financial performance. Put differently, the gap in valuation multiples is far larger than the gap in underlying business performance. In several cases, peer companies enjoy valuation premiums of 2-5x despite operating metrics that are only moderately better—or in some cases comparable—to those of 20 Microns

Vishnu Chemicals

Vishnu Chemicals has successfully positioned itself as a specialty chemicals company with strong export presence, chromium and barium chemistry capabilities, backward integration and import-substitution opportunities. Investors perceive it as a specialty chemical franchise rather than a commodity producer.

A premium valuation is understandable. However, Vishnu’s current ROCE is lower than 20 Microns’ and free cash flow generation has been affected by large expansion programmes.

The valuation gap appears wider than the underlying operating gap.

Ador Welding

Ador is viewed as an industrial technology and engineering solutions company supplying welding consumables, equipment and automation systems. The company also benefits from a strong brand and long operating history.

Its business positioning clearly attracts higher investor interest, despite financial metrics that are not dramatically superior to 20 Microns’.

TCPL Packaging

TCPL Packaging supplies packaging solutions to leading consumer brands. Packaging businesses are often viewed as beneficiaries of premiumisation, FMCG growth and long-term consumption trends.

This consumer-facing narrative supports higher valuations even though TCPL’s return profile and growth metrics are broadly comparable to 20 Microns.

HLE Glascoat

HLE Glascoat manufactures glass-lined reactors and process equipment for the pharmaceutical and chemical industries. Investors see the company as a play on pharmaceutical and specialty chemical capital expenditure.

The valuation reflects expected future opportunities rather than current profitability metrics, which have moderated in recent years.

Ratnaveer Precision Engineering

Ratnaveer manufactures stainless-steel engineering products and has delivered strong recent growth. Investors view it as a precision manufacturing and export story.

Much of the valuation premium appears to be attributable to growth expectations rather than superior return metrics.

Harsha Engineers

Harsha is one of the world’s leading bearing-cage manufacturers and operates in a highly specialised niche with global customers. The company benefits from a strong precision-engineering narrative and export franchise.

The market assigns premium valuations to businesses perceived as technology-led and globally competitive.

Rajratan Global Wire

Rajratan is a leading manufacturer of tyre bead wire, a mission-critical component in tyre manufacturing. Its products are highly engineered despite representing a small portion of customers’ overall costs.

The market recognises the strategic importance of the product and values the company accordingly.

What Is the Market Missing?

The common thread among all the peers is not the products they sell.

The common thread is how investors perceive them.

Investors see:

- Vishnu as specialty chemicals

- Harsha as precision engineering

- Rajratan as a critical automotive supplier

- Ador as industrial technology

- TCPL as a packaging franchise

Yet all these companies fundamentally supply industrial intermediates.

20 Microns also supplies industrial intermediates.

The key difference is that it remains viewed through a mining and minerals lens.

However, the company’s financial record suggests it possesses meaningful competitive advantages in:

- Application know-how

- Product formulation

- Processing capability

- Customer qualification

- Technical service

- Supply-chain reliability

These advantages are reflected in its sustained returns and cash generation.

What Could Be a Fair Valuation?

The objective is not to argue that 20 Microns should trade at the peer-group average.

The company grows somewhat slower than some peers and operates in a less fashionable segment.

However, it is equally difficult to argue that a business with:

- ~18% long-term ROCE

- Strong cash generation

- Conservative balance sheet

- Long operating history

- Consistent profitability

deserves to trade at just 9.7x earnings and 5.7x EV/EBITDA.

A more reasonable valuation framework might be:

Conservative Case

- PE: 14–16x

- EV/EBITDA: 8–10x

Fair Value Case

- PE: 18–20x

- EV/EBITDA: 10–12x

Even these ranges would leave 20 Microns trading at a discount to many specialty chemical and precision engineering peers.

Conclusion

The investment case for 20 Microns is not that it is a hidden high-growth company.

The investment case is that it is a high-quality industrial intermediate supplier that appears to be valued as a commodity producer.

Over the past decade, the company has delivered sustained returns on capital, generated substantial free cash flow, reduced leverage and grown consistently. These outcomes are difficult to reconcile with the notion of a fully undifferentiated commodity business.

The most likely explanation is that 20 Microns possesses meaningful but underappreciated competitive advantages in processing capability, formulation expertise, customer qualification, application know-how and long-standing customer relationships.

Put differently, the market appears to value 20 Microns primarily through a mining and minerals lens, whereas its operating performance suggests it should be viewed as a specialised industrial materials company.

Ultimately, the debate is not whether 20 Microns deserves to trade at the same valuation as specialty chemical or precision engineering companies. The more relevant question is whether the current valuation discount is proportionate to the differences in business quality, growth prospects and operating performance. The evidence suggests it is not. The gap in market valuation appears considerably wider than the gap in underlying operating fundamentals

This is precisely what creates the rerating opportunity. If investors begin to view 20 Microns as a specialised industrial materials company rather than a commodity mineral processor, even a partial narrowing of this perception gap could lead to a meaningful re-rating in valuation multiples.

In short, if investor perception shifts from “commodity minerals” to “value-added industrial materials”, a meaningful valuation re-rating appears possible.

Appendix: Data Comparision table

#20Microns #EquityResearch #IndustrialMaterials #IndianManufacturing

#FundamentalAnalysis #ValueCreation #InvestmentInsights #20MicronsNano

Disclaimer

Client Relationship Disclosure: Wisdomsmith Advisors LLP (“Wisdomsmith” or “We”) is an advisor to 20 Microns Limited (“Company”) on matters related to investor relations. As part of this relationship, we undertake communication with registered secondary market participants. We also convey the feedback given by market participants on matters related to business operations, financial disclosures, or corporate governance matters to the Company.

This is a document made from Public Information: This document has been made by Wisdomsmith from information made public by the Company, or the other companies mentioned in the document (typically peers of the Company). No part of this document contains confidential or non-public information.

Legal Notices and Disclaimer: This document must not be copied, reproduced, distributed, or passed to others at any time without the prior written consent of Wisdomsmith. The distribution of this document is not to be taken as any form of commitment on the part of Wisdomsmith or the Company to proceed with any transaction whatsoever. Investors and analysts reading this document should do their own analysis and form their own opinions regarding the Company. The document must be promptly returned to Wisdomsmith upon request.

None of Wisdomsmith, the Company, its subsidiaries or associate companies, its shareholders or any of their directors, officials, employees, affiliates, representatives or advisors make any representation or warranty, expressed or implied, as to the accuracy or completeness of any of the information contained, herein, including any opinion or any other written or oral communication transmitted or made available, and each recipient of such information expressly disclaims any and all liability relating to or resulting from the use of such information and communications by a recipient or any of its affiliates, advisors or representatives. In particular, no representation or warranty is given as to the achievement or reasonableness of any future projections, estimates or statements about the future prospects of any of the companies.

Copyright© 2026 Wisdomsmith Advisors LLP: All rights reserved. No part of this document may be reproduced or utilized, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying recording or otherwise, without the prior permission of Wisdomsmith.

Contact: admin@wisdomsmith.com